At Thomson Financial Partners, our goal is always the same — to help you grow your wealth and reach your goals, while doing so as efficiently as possible.

Recently, we’ve been introducing several artificial intelligence (A.I.) tools into parts of our business. This helps us serve you better and keep you informed about what we’re doing and why.

One of the most significant improvements has been transcribing our client meetings. Instead of focusing on note-taking, we can give our full attention to the conversation — asking better questions and making sure we cover what matters most. Clients have told us they love this change.

If you haven’t received one of these detailed meeting follow-up emails yet, you will soon.

To give you an idea of how we are leveraging AI in the office, we have used the notes transcribed from our recent meeting with Greg Lagasse and Grant Schneider, Partners at EdgePoint Wealth Management, to compose the rest of this Client Communication! Greg and Grant joined us in the office this week to talk about EdgePoint’s important reporting and portfolio updates, and we were able to fully engage in the conversation instead of worrying about capturing all of the important details accurately on paper.

________________________________________

💬 Financial Discussion with EdgePoint

📊 CRM3 Reporting & Active Management Value

Grant explained that CRM3, which is a regulatory initiative to increase transparency around the true costs of investing, will require reporting of both underlying product fees and advisor fees on December 31, 2026, statements.

EdgePoint has prepared materials to help advisors explain the value of active management and the accompanying fees to clients who might not understand the difference between “active” and “passive” investments.

While having a portfolio built with both passive and active investments has value, Grant noted that 80% of institutional investors (like pension plans and sovereign wealth funds) are looking to increase active management in their portfolios due to concerns about concentration risk and high valuations in passive indexes. As evidence, the S&P 500’s top 10 stocks now represent approximately 40% of the total index, with 7 out of 10 being tech stocks, creating significant concentration risk.

🌎 Market Valuations & Portfolio Positioning

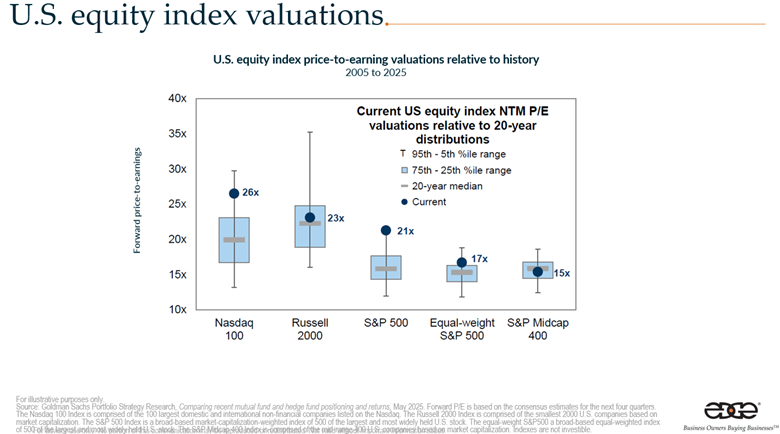

Greg presented data showing that U.S. markets are trading at premium valuations compared to historical averages. The NASDAQ is near the 95th percentile of its 20-year valuation range, while the S&P 500 is trading at 22x earnings compared to its 20-year average of 16x (34% more expensive).

The EdgePoint Global Portfolio has reduced its U.S. exposure to approximately 40% (down from 70% when EdgePoint started), as they’re finding better opportunities internationally.

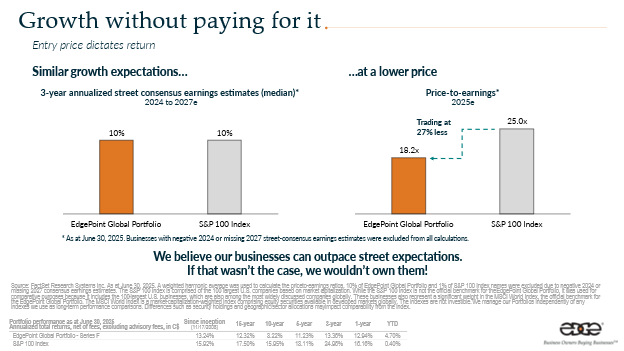

The portfolio has an active share of 98%, meaning it’s significantly different from benchmark indexes. Grant highlighted that the EdgePoint Global Portfolio offers similar earnings growth expectations to the S&P 100 but at a 27% discount in terms of valuation.

🏢 Portfolio Activity & Holdings

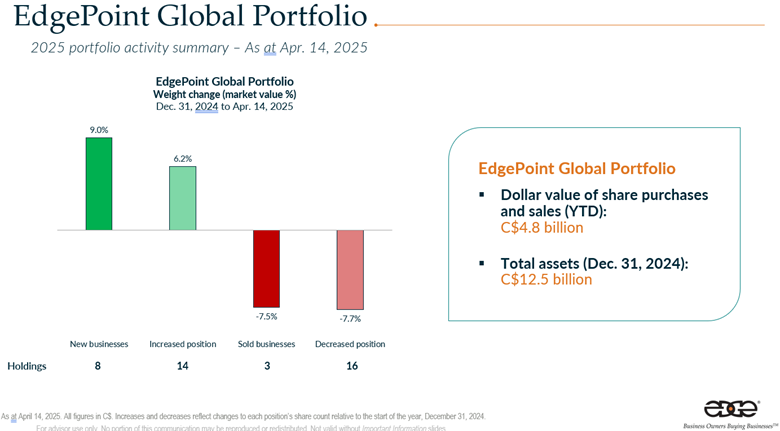

The first half of 2025 was one of EdgePoint’s busiest periods, with approximately $4.8 billion moved in the first 2.5-3.5 months following “Liberation Day” (market volatility). They’ve added 12 new businesses to the Global Portfolio this year, with 6 of the first 8 having been on long-term watch lists.

Recent portfolio activity included three buyouts of holdings: Berry Global (acquired by their largest competitor, Amcor); Norfolk Southern (acquired by Union Pacific); and Dayforce/Ceridian (being acquired by Thoma Bravo) at a premium in the mid-20% range.

Grant discussed Nippon Paint (the “Sherwin Williams of Asia”) trading at a 45% discount to Sherwin Williams despite better earnings growth; Philips, which has transformed into a pure-play healthcare business; and Warner Brothers Discovery. The portfolio’s cash position is around 7-8%, partly due to the recent takeouts mentioned above.

💵 Fixed Income Strategy

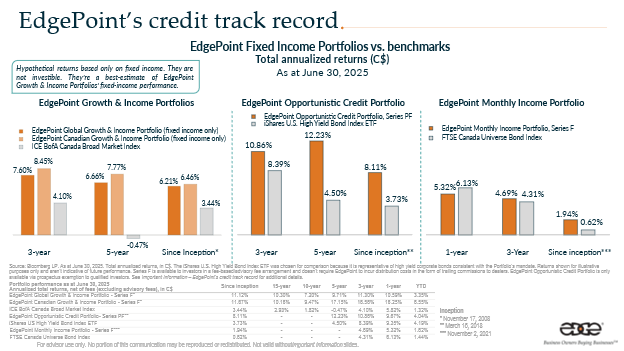

Greg and Grant briefly discussed EdgePoint’s fixed income approach; noting that their active management has delivered returns exceeding yield-to-maturity expectations, unlike many passive fixed income ETFs where actual returns significantly trail yield-to-maturity figures.

The Opportunistic Credit portfolio has a yield-to-maturity of 7.80% and has historically outperformed this metric. The fixed income portion maintains low duration to minimize interest rate risk and focuses on North American issues without using derivatives or complex products. Year-to-date, the Opportunistic Credit fund is up approximately 4% while maintaining about 20% cash position.

📌 Key takeaway: You can’t outperform the market or deliver better risk-adjusted returns if you look like the market.

💡 Why This Matters to You

Understanding where opportunities — and risks — exist in today’s markets helps ensure your portfolio is positioned for long-term success. By partnering with managers like EdgePoint, who actively seek undervalued opportunities and avoid market concentration, we aim to protect your investments while still pursuing attractive returns. This disciplined, research-driven approach is a key reason your portfolio is built to handle both current market conditions and future changes.

________________________________________

At Thomson Financial Partners of Assante Capital Management Ltd, we’ll keep using our time, technology, and resources in ways that deliver real value to you — because that’s what you deserve.

Note: slides were added to the summary that A.I. provided.

At Thomson Financial Partners, our goal is always the same — to help you grow your wealth and reach your goals, while doing so as efficiently as possible.

Recently, we’ve been introducing several artificial intelligence (A.I.) tools into parts of our business. This helps us serve you better and keep you informed about what we’re doing and why.

One of the most significant improvements has been transcribing our client meetings. Instead of focusing on note-taking, we can give our full attention to the conversation — asking better questions and making sure we cover what matters most. Clients have told us they love this change.

If you haven’t received one of these detailed meeting follow-up emails yet, you will soon.

To give you an idea of how we are leveraging AI in the office, we have used the notes transcribed from our recent meeting with Greg Lagasse and Grant Schneider, Partners at EdgePoint Wealth Management, to compose the rest of this Client Communication! Greg and Grant joined us in the office this week to talk about EdgePoint’s important reporting and portfolio updates, and we were able to fully engage in the conversation instead of worrying about capturing all of the important details accurately on paper.

________________________________________

💬 Financial Discussion with EdgePoint

📊 CRM3 Reporting & Active Management Value

Grant explained that CRM3, which is a regulatory initiative to increase transparency around the true costs of investing, will require reporting of both underlying product fees and advisor fees on December 31, 2026, statements.

EdgePoint has prepared materials to help advisors explain the value of active management and the accompanying fees to clients who might not understand the difference between “active” and “passive” investments.

While having a portfolio built with both passive and active investments has value, Grant noted that 80% of institutional investors (like pension plans and sovereign wealth funds) are looking to increase active management in their portfolios due to concerns about concentration risk and high valuations in passive indexes. As evidence, the S&P 500’s top 10 stocks now represent approximately 40% of the total index, with 7 out of 10 being tech stocks, creating significant concentration risk.

🌎 Market Valuations & Portfolio Positioning

Greg presented data showing that U.S. markets are trading at premium valuations compared to historical averages. The NASDAQ is near the 95th percentile of its 20-year valuation range, while the S&P 500 is trading at 22x earnings compared to its 20-year average of 16x (34% more expensive).

The EdgePoint Global Portfolio has reduced its U.S. exposure to approximately 40% (down from 70% when EdgePoint started), as they’re finding better opportunities internationally.

The portfolio has an active share of 98%, meaning it’s significantly different from benchmark indexes. Grant highlighted that the EdgePoint Global Portfolio offers similar earnings growth expectations to the S&P 100 but at a 27% discount in terms of valuation.

🏢 Portfolio Activity & Holdings

The first half of 2025 was one of EdgePoint’s busiest periods, with approximately $4.8 billion moved in the first 2.5-3.5 months following “Liberation Day” (market volatility). They’ve added 12 new businesses to the Global Portfolio this year, with 6 of the first 8 having been on long-term watch lists.

Recent portfolio activity included three buyouts of holdings: Berry Global (acquired by their largest competitor, Amcor); Norfolk Southern (acquired by Union Pacific); and Dayforce/Ceridian (being acquired by Thoma Bravo) at a premium in the mid-20% range.

Grant discussed Nippon Paint (the “Sherwin Williams of Asia”) trading at a 45% discount to Sherwin Williams despite better earnings growth; Philips, which has transformed into a pure-play healthcare business; and Warner Brothers Discovery. The portfolio’s cash position is around 7-8%, partly due to the recent takeouts mentioned above.

💵 Fixed Income Strategy

Greg and Grant briefly discussed EdgePoint’s fixed income approach; noting that their active management has delivered returns exceeding yield-to-maturity expectations, unlike many passive fixed income ETFs where actual returns significantly trail yield-to-maturity figures.

The Opportunistic Credit portfolio has a yield-to-maturity of 7.80% and has historically outperformed this metric. The fixed income portion maintains low duration to minimize interest rate risk and focuses on North American issues without using derivatives or complex products. Year-to-date, the Opportunistic Credit fund is up approximately 4% while maintaining about 20% cash position.

💡 Why This Matters to You

Understanding where opportunities — and risks — exist in today’s markets helps ensure your portfolio is positioned for long-term success. By partnering with managers like EdgePoint, who actively seek undervalued opportunities and avoid market concentration, we aim to protect your investments while still pursuing attractive returns. This disciplined, research-driven approach is a key reason your portfolio is built to handle both current market conditions and future changes.

________________________________________

At Thomson Financial Partners of Assante Capital Management Ltd, we’ll keep using our time, technology, and resources in ways that deliver real value to you — because that’s what you deserve.

Note: slides were added to the summary that A.I. provided.

Archives

Categories